Lenders across the country, including three of Canada’s Big 6 banks, are once again busy slashing fixed mortgage rates—a welcome sign for those facing renewal in the coming months.

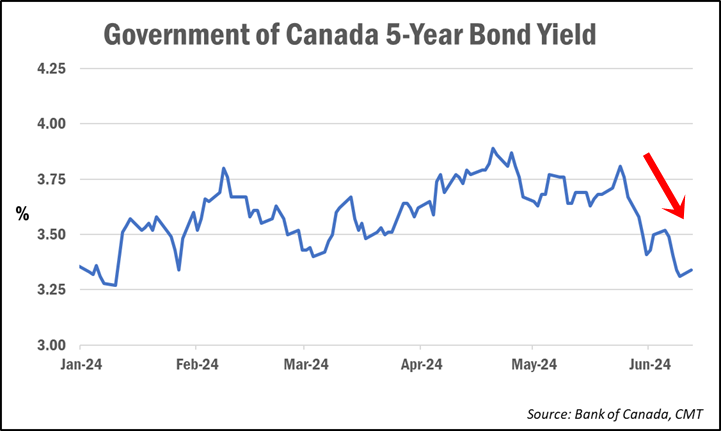

As we reported last week, lenders had already started trimming rates in the wake of a nearly 40-basis-point drop in bond yields, which typically lead fixed mortgage rate pricing.

While none of the big banks made any major rate moves at that time, this week saw BMO, CIBC and RBC all deliver widespread rate reductions to their posted special rates across all mortgage terms. The rate drops averaged around 10-15 basis points, but in some cases amounted to cuts in excess of 20 bps (0.20%), according to data from MortgageLogic.news.

“It’s great news for people who are renewing,” rate expert Ron Butler of Butler Mortgage said in a social media post.

In particular, the recent rate cuts are likely welcome relief for the 76% of mortgage holders facing renewal in the coming 12 months who say they are anxious about the process, as revealed in Mortgage Professionals Canada’s latest consumer survey.

“Rates are going from mostly all 5%-plus, to mostly rates in the [4%-range],” Butler noted.

While shorter terms like the 1- and 2-year fixeds are continuing to be priced a little bit higher, Butler says most 3- and 5-year terms will be available for under 5%.

While there are now 5-year-fixed high-ratio (less than 20% down payment) rates available in the 4.50%-range, Butler says those with renewals who typically require an uninsured mortgage (with a down payment of greater than 20%) can expect rates ranging from 4.79% to 4.99%.

“The bottom line is there’s finally some relief coming. Praise be,” he said.

The rate reductions follow a continued decline in Canadian bond yields,

Bruno Valko, Vice President of National Sales at RMG, told CMT the move largely coincides with similar movements south of the border, with both markets reacting to the latest lower-than-expected inflation results in both Canada and the U.S.

“As the 10-year [U.S.] Treasury yield goes, the 5-year Government of Canada yield follows,” he said.

Mortgage broker and rate expert Ryan Sims predicts that this latest round of rate cuts will start to open up some differentiation in rate pricing between lenders.

“Everyone has different risk levels, different exposures, and different profit targets on their mortgage book,” he told CMT. “So I think, for the first time in a while, we will see a nice spread between the same rate lender to lender.”

He expects some mortgage lenders will focus on insurable mortgages, while others will compete on uninsurable products, all in pursuit of “fatter margins.”

“It will be interesting to see where the chips fall on this, but I think finally lenders will have a different spread, which we have not seen for a while,” he said.

And while reluctant to speculate where rates could head from here, Sims suggests we could potentially see continued rate declines over the next 30 to 60 days, with an eventual pull-back in response to bad economic data.

“Basically, like waves on the ocean, we go up and we go down, but we are range-bound at the floor of about 3.05% and a ceiling around 3.75% [for the 5-year bond yield],” he said. “Until we see definitive data one way or the other to break out of the range, we hold this up and down pattern.”

Falling mortgage rates could help soften the payment shock expected for the estimated 2.2 million mortgages that will be renewing at higher rates in the next two years.

However, Butler warns that just because mortgage rates are falling doesn’t mean all lenders will be offering equally low rates in their renewal letters.

“If you’ve got a renewal coming up…they’re sending you a letter now that’s got a kind of high rate, so you’ve got to fight back [and argue] that rates are coming back down,” he said. “They don’t just hand [out their best rates]. You’ve got to do your research.”

Butler recommends borrowers visit rate comparison sites to become better informed about the current rates that are available elsewhere. He says the information can then be used as leverage when negotiating with your lender, even if you don’t intend on switching.

Unfortunately, it appears many homeowners are doing less haggling at renewal, despite being faced with higher interest rates. The same MPC study cited above revealed that 41% of borrowers accepted the initial rate offered by their lender at renewal.

A shockingly low 8% said they “significantly” negotiated their rate at renewal.

However, one big factor that could be preventing many borrowers from trying to negotiate their rate is the fact that they’ve become “trapped” at their existing lender thanks to the mortgage stress test—and they know it.

The Office of the Superintendent of Financial Institutions (OSFI) applies the mortgage stress test to uninsured borrowers when switching lenders. This forces them to re-qualify at an interest rate priced two percentage points above their contract rate, limiting their options and reducing their leverage for negotiating better terms, especially if their financial situation has changed.

Just last week, OSFI head Peter Routledge rejected renewed calls to remove the mortgage stress test from uninsured mortgage switches.

“From our perspective, the rules—from an underwriting standpoint—make sense to us. If you’re taking credit risk anew, you’re re-underwriting,” he said.