While the homebuilders weren’t surprised by the better-than-estimated new home sales report released Friday, some people were a bit shocked. But the forward-looking purchase application data was getting better from Nov. 9 up until the early part of February as mortgage rates fell from 7.37% to 5.99%. Now, of course, that has all changed quickly.

On CNBC Friday morning, I highlighted that whatever data stabilization we had at 5.99%, it’s now gone in the blink of an eye.

The homebuilders are crafty people (pun intended). They move homes like they are commodities, not as a secured form of shelter they live in. They don’t ever have to have the conversation about how low their total payment is in the new home they’re buying, unlike some of their buyers (which explains higher cancellation rates).

To combat higher mortgage rates, builders have been cutting prices and buying down rates to move product. They still have a lot of work to do here, so we shouldn’t expect anything good to come from the housing permits side of the economy in 2023.

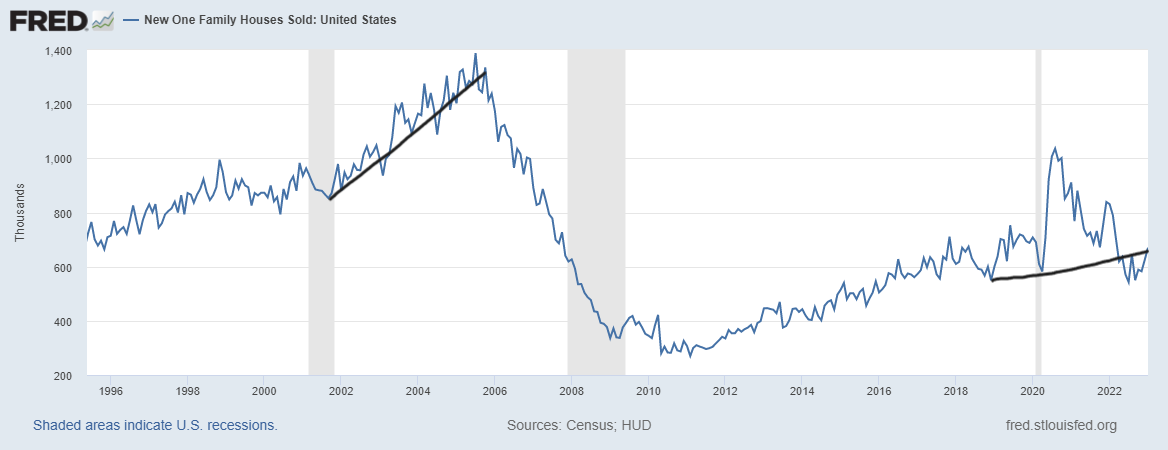

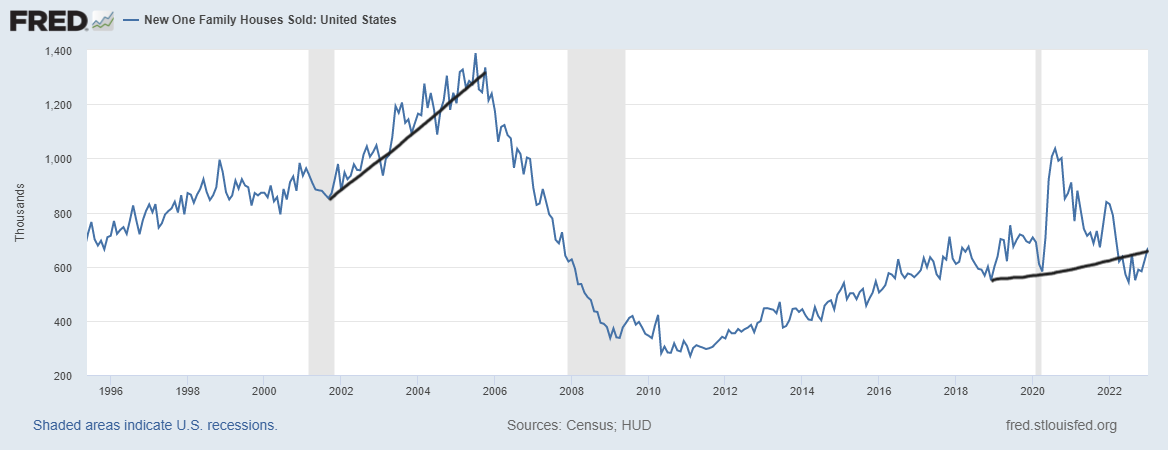

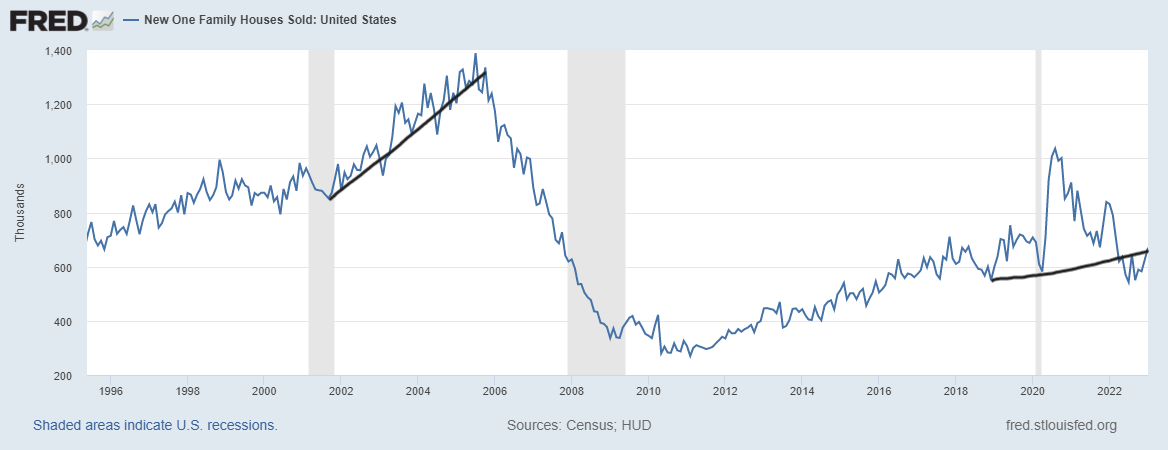

From Census: Sales of new single-family houses in January 2023 were at a seasonally adjusted annual rate of 670,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 7.2 percent (±20.4 percent)* above the revised December rate of 625,000, but is 19.4 percent (±13.1 percent) below the January 2022 estimate of 831,000.

As I have stressed for months, the new home sales levels are historically low and don’t account for the cancellation rate. Just like in the existing home sales market, when sales are low, anything positive on the rate side can move the market in a positive direction.

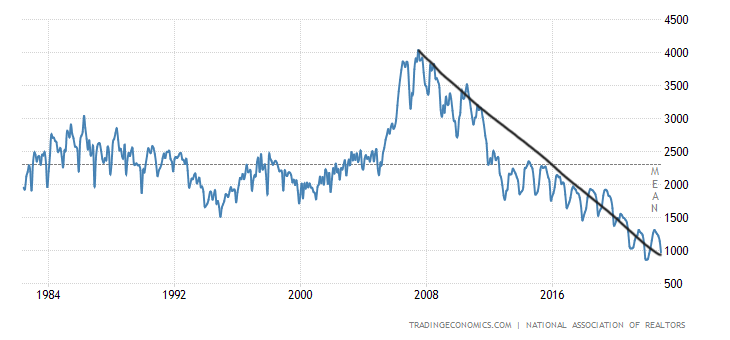

This goes into my low housing bar theme for 2023 and why we need context with sales data. If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether. As we can see in the chart below, we are still below the recession levels of 2000 and really trending at 1996 levels. And we have a lot more workers now than we did then.

I wouldn’t read too much into the fact that this new home sales report beat estimates, but I would say that in the future, if mortgage rates get back toward 6%, the homebuilders have creative ways to sell their homes that the existing home seller might not be inclined to do.

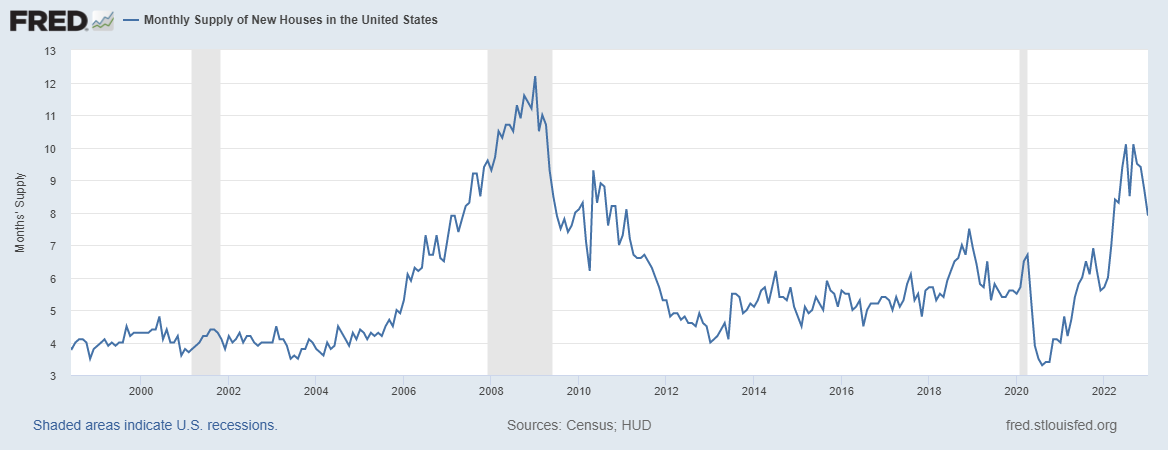

The seasonally-adjusted estimate of new houses for sale at the end of January was 439,000. This represents a supply of 7.9 months at the current sales rate.

This is a positive trend: the homebuilders are working through their supply and while their monthly supply levels are still too high to issue new permits, we are making progress here.

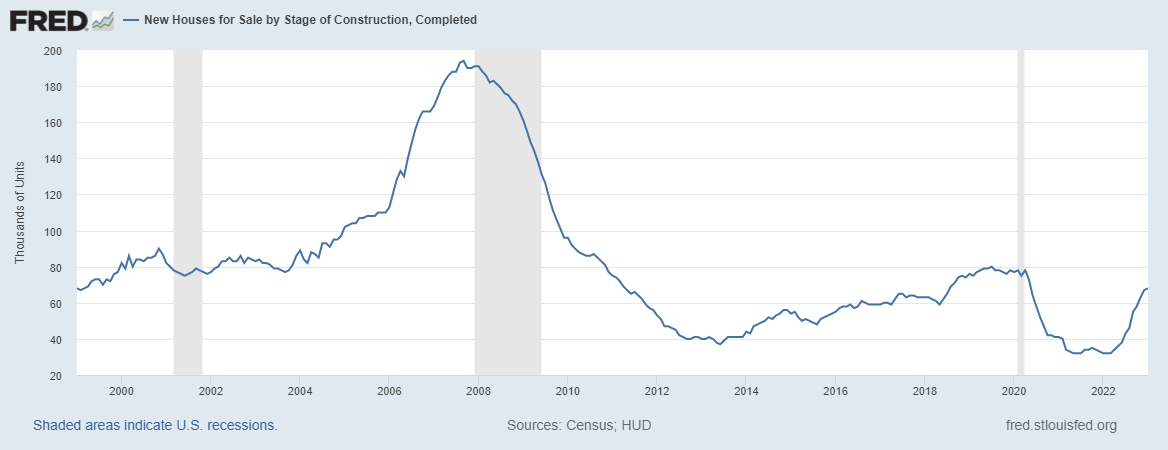

However, some context is needed here as well. Here is a breakdown of the supply data:

One of the most incorrect parts of the housing inventory story lately is that we have a record number of homes under construction and that the builders are about to flood the housing market with a massive number of homes on the scale of 2008. However, this isn’t how inventory grows in America.

The majority of inventory comes from the existing home sales market and if you compare it to 2008, back then we didn’t even have 200,000 homes available for sale and currently we are at 68,000.

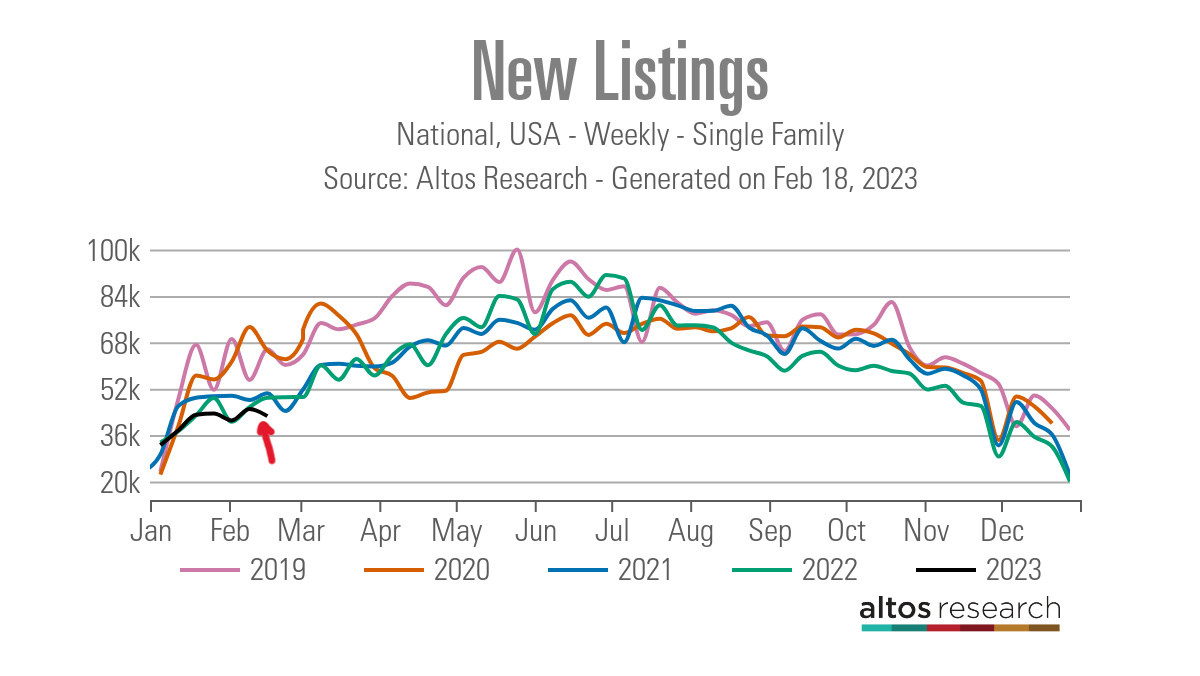

When we look at active listings today, we are still at 980,000, near all-time lows, even with the recent massive hit to demand. To get more inventory you need more Americans to list their homes.

As we can see with the new listing data, not much is going on here:

For the homebuilders to start building new homes, I have a very simple model. My rule of thumb for anticipating builder behavior is based on the three-month supply average. This has nothing to do with the existing home sales market; this monthly supply data only applies to the new home sales market, and the current nine months are too high for them to issue new permits.

As you can see, the builders still have a lot of work to do before considering a new housing cycle, so the sector is still in a recession while working off the backlog. They’re lucky that active listings are so low, which gives their product more value.

So, all in all, yes, the new home sales beat estimates, but that was in a lower-mortgage-rate world. Now that rates have spiked up almost 1%, we’ll see how much more buydowns homebuilders will need to do to keep this progress going.

Suppose mortgage rates had broken below 5.75%. In that case, we would be having a different conversation today. However, as part of my 2023 forecast, as long as the economy stays firm, I believe the 10-year yield range should be between 3.21%-4.25%, which means rates between 5.75%-7.25%. So far as the economic data has stayed firm, the bond yield range looks right to me.

The housing market story is about where the 10-year yield is going. Credit standards are still looking great, and we don’t have to worry about credit getting so tight that it will kill demand, as we saw from 2005 to 2008.

It will be a long grind for homebuilders to get the current stock off their books. However, we have seen what can happen when mortgage rates get below 6%, so we need to be patient while the Fed tries to slow the economy down fast enough to bring inflation down.